Business Vertical Classification Categories: A Strategic Guide for Startups

Here’s something I see constantly. A founder fills out a government form, picks “software” from a dropdown, and considers the vertical question answered. Then six months later, they wonder why their investor conversations keep going nowhere.

The vertical you claim isn’t a filing decision. It’s a positioning decision. It changes which investors call you back, which customers trust you on first contact, which regulations apply to you, and how your metrics get benchmarked.

I’ve watched a payments startup miss an entire wave of fintech-focused VCs because they kept calling themselves “tech.” I’ve watched a telehealth company confuse generalist SaaS investors who needed ARR multiples to evaluate it, not healthcare outcomes data. Classification isn’t passive. It actively shapes the conversations you get into.

This is a guide to doing it deliberately instead of by accident.

Vertical vs Sector: Why the Distinction Matters

A sector is broad. Technology. Healthcare. Finance. Those are sectors.

A vertical is specific. Telehealth within healthcare. B2B cybersecurity within technology. Embedded payments within fintech. The vertical tells you which customers you’re serving, what their buying process looks like, and what they actually care about.

The distinction matters because investors, buyers, and regulators all operate at the vertical level, not the sector level. A healthcare-focused VC isn’t the same as a tech-focused VC. A HIPAA compliance requirement isn’t an SOC 2 requirement. A hospital procurement process isn’t a SaaS land-and-expand motion. When founders talk in sector terms, and everyone else is thinking in vertical terms, mismatches happen at every stage of the business.

Vertical vs Horizontal: The Salesforce and Veeva Example

This is the foundational question most founders never explicitly answer.

A vertical business serves a specific industry. A horizontal business serves everyone. Both are legitimate strategies. They are not equally good for early-stage startups with limited resources.

Veeva Systems is an example worth studying. Salesforce was building a horizontal CRM for every industry. Veeva looked at life sciences specifically and built a CRM designed for exactly how pharmaceutical companies and biotech firms work: sales cycles, regulatory workflows, compliance documentation, clinical data management, all of it built for one vertical.

The results were stark. Veeva reached $1 billion in revenue faster than Salesforce did, despite a fraction of the addressable market. Their customer churn is lower. Their competitive moat is nearly impossible to attack from the outside because the domain expertise required to compete with them isn’t something you replicate quickly.

Here’s how the two approaches compare directly:

| Dimension | Salesforce (Horizontal) | Veeva Systems (Vertical) |

| Market approach | CRM for every industry across all sectors | CRM built exclusively for life sciences |

| Target customer | Any company that needs customer management | Pharmaceutical, biotech, and medical device firms |

| Time to $1B revenue | 10 years after founding | 7 years after founding (faster despite smaller TAM) |

| Gross margin | Around 73-75% | Around 72-74% (comparable despite niche focus) |

| Customer churn | Higher churn risk across diverse customer types | Very low churn due to deep workflow integration |

| Competitive moat | Brand, scale, ecosystem of integrations | Domain expertise that generalists can’t replicate quickly |

| Regulatory depth | General data security and compliance | Built-in FDA 21 CFR Part 11, GDPR for pharma, GxP compliance |

| Expansion path | Horizontal expansion across more product categories | Vertical expansion deeper into life sciences workflows |

| Key lesson for startups | Horizontal scale requires significant resources and brand to win across verticals | Vertical specificity creates faster credibility, stronger retention, and a defensible moat with fewer resources |

For early-stage startups, the resource constraint makes the choice clearer. You can’t build deep credibility everywhere. You can build it somewhere. Pick the vertical where your team has the most knowledge, the problem is sharpest, and competition is thinnest.

The Four Classification Systems You’ll Actually Encounter

Each was built for a different purpose and serves a different audience. Knowing which one you’re dealing with saves time and prevents confusion.

1. NAICS: North American Industry Classification System

NAICS is the US government standard for regulatory reporting, tax filings, government contracts, and grant applications. If you’re applying for SBIR grants or doing government procurement, you need a NAICS code. Six digits, running from broad sectors at two digits down to specific industries at six. The more specific your code, the better your grant and procurement matching.

2. SIC: Standard Industrial Classification

Old. Designed in the 1930s, last updated in 1987. No cloud computing, no standalone biotech, no digital-native anything. Some legacy financial databases still reference it. Use it only when something specifically requires it.

3. GICS: Global Industry Classification Standard

Developed by MSCI and S&P for investment analysis. Eleven sectors, 25 industry groups, 74 industries, 163 sub-industries. When investors talk about public comparables or peer benchmarks, they’re working within GICS logic. Knowing where you’d land helps you understand which public companies investors are using to benchmark you.

4. ICB: Industry Classification Benchmark

Used by major stock exchanges for cross-market analysis. More granular than GICS at 173 subsectors. More relevant if you’re raising from European or cross-border institutional investors.

| System | Purpose | Who Uses It | Last Updated | Best For Startups |

| NAICS | Government and regulatory reporting | Tax agencies, procurement offices | Every 5 years | Compliance, grants, government contracts |

| SIC | Legacy industrial classification | Older financial databases | Last updated 1987 | Historical comparisons only |

| GICS | Investment analysis and benchmarking | Institutional investors, analysts | Quarterly | Benchmarking against public comparables |

| ICB | Stock exchange cross-market analysis | Global exchanges, fund managers | Annual | Cross-border investor conversations |

Practical implication: NAICS for government interfaces, GICS for investor conversations, and know your primary vertical, regardless of which formal system the other person is using.

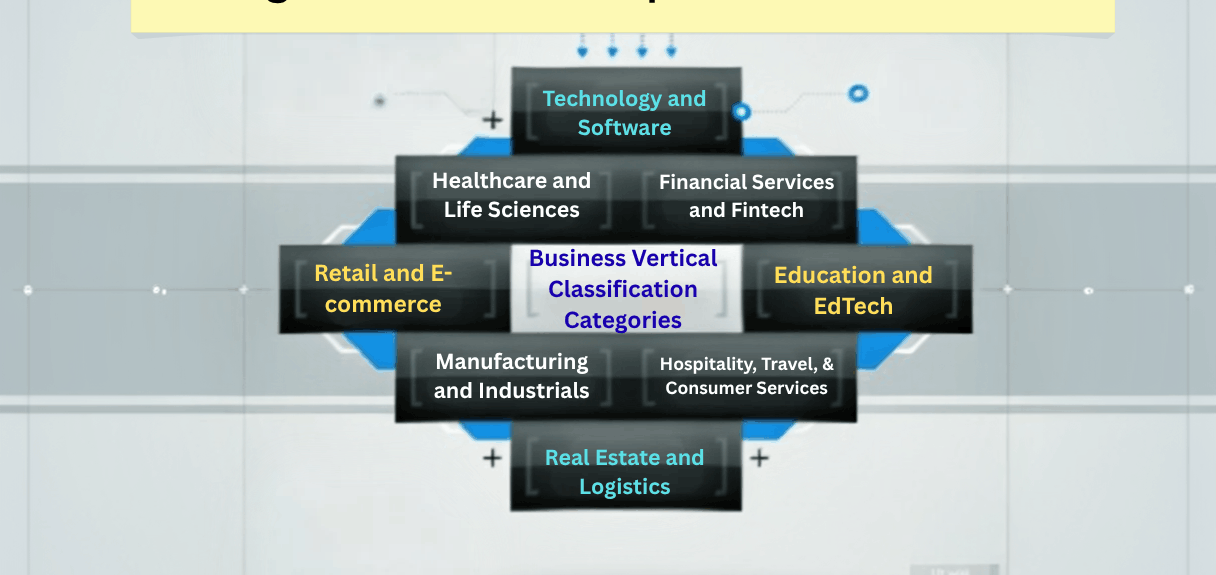

The Seven Major Verticals and What Each Means for a Startup

1. Technology and Software

The broadest one and the trap most founders fall into. Hardware, software, cloud, AI, cybersecurity, and IT services. It’s so wide it tells nobody anything. “I’m building a tech startup” is not a vertical position.

Go deeper. Enterprise SaaS. Developer tools. Infrastructure. B2B cybersecurity. Consumer mobile. The sub-vertical is where the useful signal lives. Investors who specialize in enterprise SaaS think completely differently from investors who specialize in consumer apps.

2. Healthcare and Life Sciences

Regulated, slow to sell into, genuinely worth it once you’re embedded. Churn is low when you’re in clinical workflows. NRR runs higher than most other verticals because switching costs are real.

3. Financial Services and Fintech

Banks, insurers, investment firms, and everything being built on top of or in reaction to them. Compliance posture and licensing requirements are load-bearing from day one. The early structural decision: are you replacing incumbents, partnering with them, or serving them? That choice determines your go-to-market and your investor profile.

4. Retail and E-commerce

Physical and digital commerce, logistics, payments, and the software running all of it. Margins are thinner than B2B. CAC is high. But feedback loops are faster than almost any other vertical, and the market is enormous. A startup with a clear ROI story around conversion or margin improvement has a relatively direct buyer conversation.

5. Education and EdTech

Real demand, genuinely hard to sell. K-12 is budget-constrained and slow. Higher ed moves more slowly. Corporate L&D is more nimble but fragmented. Valuations in this space compressed after the pandemic bubble. The underlying need is real, but the funding environment and sales motion are both harder than in other verticals right now.

6. Manufacturing and Industrials

Slow sales cycles, relationship-dependent buying, and very high retention once embedded. This vertical is underserved by software relative to its size. Industrial IoT, predictive maintenance, and supply chain software are genuinely disrupting industries that haven’t changed much in decades. Founders with real manufacturing domain expertise can build significant businesses here.

7. Hospitality, Travel, and Consumer Services

High macro sensitivity, rebuilt after significant disruption, and still early in the digital transformation of core operations. Loyalty systems, booking infrastructure, and operations management are all getting rebuilt. The opportunity is real for startups that can navigate an industry where trust and relationships often matter more than feature sets.

Why Getting This Wrong Costs Real Money

Misclassification isn’t a paperwork problem. The consequences are compound.

CurrentHabit: highlights that investor misalignment is the most expensive mistake. VC funds specialize by vertical more than founders realize. A healthcare-focused fund has healthcare-specific metrics, clinical advisor networks, and relationships with healthcare-focused growth funds. Pitch them a fintech company, and they literally don’t have the right frame to evaluate it. The pass isn’t a judgment on the business quality. It’s a structural mismatch.

Techbonna: explains that benchmarking errors compound across multiple fundraisers. Investors compare your metrics to your vertical peers. A B2B cybersecurity company with 120% NRR looks strong. A consumer app with the same number looks exceptional. A healthcare company with 90% NRR looks acceptable given workflow stickiness. Put the wrong company in the wrong comparison set, and the numbers tell a false story in either direction.

ThePocketJournal: documents that tech startups inadvertently operating in financial services without banking licenses have faced real enforcement actions. Getting the vertical right early tells you which regulatory bodies are watching you before a problem forces your hand.

Marketing misalignment is slower but just as costly. A law firm CRM and an e-commerce CRM are the same product category. The buyer is completely different. The vocabulary is different. The pain points are different. Generic positioning doesn’t convert in either direction.

When Your Business Doesn’t Fit One Box

Most startups doing interesting things live at the intersection of two verticals. A telehealth startup using AI to analyze patient data. A fintech company offering embedded payments for retailers. A construction software company using computer vision for safety monitoring.

Dobrev-nina.com frames the question well: what problem are you fundamentally solving, and who experiences it? If the problem is a healthcare problem and technology is how you solve it, you’re a healthcare company. If you’re building a technology platform that healthcare happens to be one use case for, you’re a tech company. The answer changes your compliance posture, investor targeting, sales motion, and who you hire.

Signs you’ve got the wrong primary vertical:

• Investor meetings end in confusion rather than a clear yes or no

• Marketing generates traffic but not qualified leads

• You’re spending significant time explaining to buyers why your category is relevant to them

• Your team’s expertise doesn’t match what buyers expect from someone in your space

• Competitor research keeps surfacing companies you’d never actually face in a real deal

How to Actually Pick Your Vertical

Five questions that cut through the noise. Answer them honestly, and the right vertical usually surfaces.

• Who is your primary customer, specifically? A job title, an industry, a company size. Not ‘enterprises.’ An actual person in an actual type of organization. The vertical lives in the honest answer to this

• What regulatory context governs their buying decision? HIPAA for healthcare. Banking compliance for fintech. FDA for medical devices. If their compliance requirements shape how they evaluate and buy from you, that context is your vertical

• Which investors actually fund companies like yours? Look at who recently funded your two or three most direct competitors. The funds that keep showing up are your vertical’s investor ecosystem

• Who do your customers actually evaluate you against? The competitors in those deals are your vertical peers. Their positioning tells you how the market categorizes the problem you’re solving

• Where does your founding team have the deepest credibility? Domain expertise builds trust with buyers faster than anything else. That credibility doesn’t transfer cleanly across verticals without significant investment

FAQs about Business Vertical Classification Categories

The sector is the top level: Technology, Healthcare, Finance. A vertical is what you actually operate within that sector. B2B cybersecurity is a vertical within technology. Telehealth is a vertical within healthcare. Investors, buyers, and regulators all operate at the vertical level. Saying you’re in ‘technology’ is technically true but practically useless for positioning.

Most due to some degree. But you need one primary vertical for practical purposes. Two verticals mean two go-to-markets, two investor audiences, two compliance frameworks, two sets of buyer vocabulary. Early-stage companies rarely have the resources to do all of that well at once. Pick one. Expand deliberately later when you have the resources to do it properly.

Investors benchmark your metrics against vertical peers. The same NRR number looks different in healthcare versus consumer apps versus enterprise SaaS. If your classification drops you into a comparison set where your metrics look weak, you’ll get comped against a lower valuation baseline even if your absolute numbers are strong. This isn’t theoretical. It comes up in every competitive fundraiser.

When your primary customer type changes. When a competitor reframes the category. When you enter an adjacent market that’s genuinely different from your first one. When regulatory changes shift the compliance landscape you’re operating in. Don’t let it drift informally. Make the decision explicitly at each meaningful growth stage.

Defaulting to the broadest possible description to avoid limiting themselves. ‘We’re in tech’ feels safe because it doesn’t exclude anyone. But it doesn’t attract anyone either. Vertical specificity is what gets you into the right conversations. Broad positioning is what keeps you out of them.

Bottom Line

Vertical classification reads like housekeeping. It isn’t.

The vertical you pick is the context everyone else uses to interpret what you’ve built. Investors use it to benchmark you. Customers use it to decide whether to trust you. Regulators use it to decide what rules apply. Competitors use it to decide whether to take you seriously.

Getting it right doesn’t require certainty about every edge case. It requires enough clarity to walk into conversations where the person across the table immediately understands who you serve and why you’re credible serving them.

Pick it deliberately. Revisit it as your business evolves. When you’re stuck, go back to the simplest version: who is your customer, what problem are you solving, and who has the most relevant frame of reference to evaluate whether you’re solving it well.

Read Also:

tags

Richard Watson

Richard Watson is a dynamic author on finance and business. He lives in New York City. Who has been winning hearts and minds with his 10+ years of experience, expertise, and blogging. With a Bachelor of Arts in Business (BA) & MCA (Master's in Computer Applications), he transforms complex financial concepts into accessible insights that resonate with both seasoned professionals and novices. His notable work has established him as an expert, guiding businesses to thrive in the digital world. He is currently on Content Operations Associate | MoneyOutlined.com & MostValuedBusiness.com